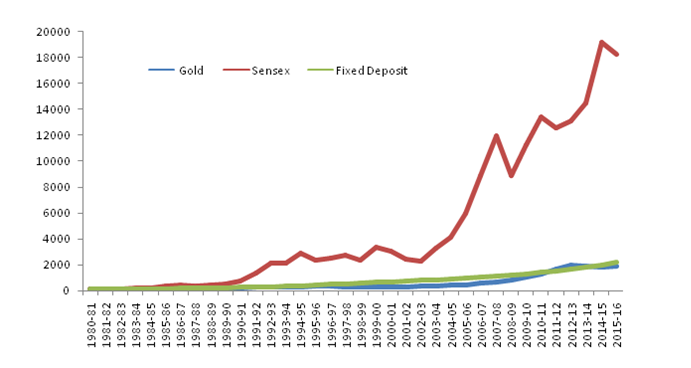

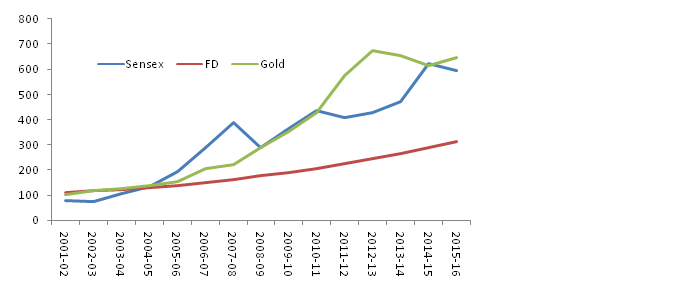

You work really hard to earn your money. But your money is having a good time in your bank account. Does it not have to work hard for you? We are talking about saving your money in the banks.

Even though it is more than two years since the Reserve Bank of India deregulated interest rates on savings deposits, most banks still offer around 4 per cent. Some banks offer higher interest rates on savings accounts but ask for a higher minimum deposit. Still, we park a significant proportion of our spare cash in these low-yielding savings accounts, earning much lower rates than the inflation rate.

Liquid funds can help us earn much higher rates than what the savings deposits offer without compromising too much on how quickly we can get our hands on the cash.

What is a liquid fund?

Liquid fund is a category of mutual fund which invests primarily in money market instruments like certificate of deposits, treasury bills, commercial papers and term deposits. Lower maturity period of these underlying assets helps a fund manager in meeting the redemption demand from investors.

But these are plain technical jargon. To a layman, it is utterly confusing. You simply need the answers to the following three questions that concern you the most.

1.Will my money be safe in liquid mutual funds?

2.Why Liquid funds are better than savings account?

3.Does it give me better Returns on Investment than storing my money away in a bank fixed deposit?

Here are the answers to your questions-

ANS1. Will my money be safe in liquid mutual funds?

Your money is primarily invested in short term instruments and the risk is quite less compared to other short term and long term debt funds; this scheme invests in the same paper as your bank would do.

You can have your money back in a working day’s notice and in some cases instantly (upto Rs. 2,00,000/-). All you have to do is pop in a redemption request, and your money is credited to your bank account.

ANS2. Liquid funds are better than savings account for following reasons-

- They provide superior returns over savings account, in general top performing liquid fund can give you anything between 1-2 % higher return

- At the same time it is as liquid as Saving account money, money can be credited to you in 24 hours, and does not carry too much risk.

- There is no exit load

ANS3. Does it give me better Returns on Investment than storing my money away in a bank fixed deposit?

With a Fixed Deposit account, you can make premature withdrawals in multiples of Rs. 1,000 subject to applicable charges, get a Loan or overdraft up to a certain percentage of your FD amount and choose from monthly or quarterly payouts. But the process with liquid funds is hassle free; you just have to pop a request and you have the money in your account the very next day and in some cases instantly (upto Rs. 200000/-). The best part is that it does not have any exit penalties.

Your liquid fund scheme earns you a return on investment that matches the offerings of the market at the time. Usually, it is more than your bank’s rate of interest, for the last one year it is 7.35%.

So what are you waiting for? Contact Equest Capital to open your liquid funds account now.

Invest in mutual funds save more.

![CropperCapture[3]](http://equestcapital.com/wp-content/uploads/2016/10/CropperCapture3.jpg)

![CropperCapture[4]](http://equestcapital.com/wp-content/uploads/2016/10/CropperCapture4.jpg)